National Lockdown Day

March 16 needs to go down in history

Something must be done to recognize this day, March 16. It was the day that “15 Days to Flatten the Curve” was announced in the US and spread to the rest of the world. The hammer really came down in a press conference question-and-answer period. We have reconstructed these dreadful 70 seconds, with videos you can watch.

Let’s all spread this message. The day needs to be marked in history. Everything that has happened since traces to this day. That includes the ongoing banking crisis. Below we publish in full a piece by our president Jeffrey Tucker that ran in Epoch Times today.

And by the way, Brownstone material appears in many venues, including the Wall Street Journal just this week, and the New York Post too. We are thrilled about the reach of our publications and research.

Sadly, we received notice today of another very important scientist fired from her job and in need of a Brownstone fellowship, which we cannot afford right now. We are already up to 9 fellows. We simply cannot do more for now. As always, we need your support.

Here is some content since our last email, which was only yesterday, followed by the promised article on banking.

A Brief History of Stolen Lives BY MARK OSHINSKIE. Very few who aggressively supported the futile, destructive “mitigation” measures have admitted that they’ve been wrong throughout. The few who have belatedly admitted this absolve themselves by falsely insisting they “couldn’t have known” that these interventions would cause serious, lasting damage.

There is No Cure for Washington’s Arrogance BY JAMES BOVARD. Most Washingtonians I meet are color blind to other people’s freedom. At the start of the pandemic, government officials trumpeted terrifying statistical extrapolations of potential infection rates. Thus, they automatically became entitled to lock people in their homes, shut down their businesses, and padlock their churches. The credentials of experts receive infinitely more respect inside the Beltway than Americans’ constitutional rights.

Balaji Srinivasan: The Man Who Was Fired Up for Covid BY MICHAEL SENGER. Unlike Tomás Pueyo, it’s unlikely that Balaji’s Twitter prophecies had a major effect on policy—though he did spread a bit of panic to bring these outcomes about. Rather, aside from the uncanny global coordination we observed in COVID policies and propaganda, Balaji’s tweets might be the best evidence so far that this plan to recreate China’s response did, in fact, exist, down to the particular terms and details of how the world would transform.

Pandemics are Not the Real Health Threat BY DAVID BELL. Saving society from eating itself with fear and stupidity will rely on us educating ourselves. Society’s ‘experts’ are doing very well from pandemics, and have no incentive to provide such education. This will require each of us to find time. Time for discussion, time for self-reflection, and time for thought on what life actually is. We need to calmly sum up what is happening around us, and take the risk of exploring what it is that we really value. Then we can stop others from abusing our ignorance.

Bonfire of the Covid Vanities BY GABRIELLE BAUER. Freedom to take a walk on the beach? Stop killing the vulnerable! Freedom to earn a living? The economy will recover! The demotion of freedom—that noble ideal of liberal democracy—to a caricature has been painful to observe. Without freedom, we have nothing resembling a life. Pandemic or not, freedom needs a place at the discussion table.

The Pandemic of Journalistic Malfeasance BY RAMESH THAKUR. Thanks to the Lockdown Files, we now have “definitive” proof that much of Covid policy was cruel and inhumane, made on the hoof, driven by dogma and self-interest, without the requisite evidence and sometimes even against scientific advice, to foment fear, avoid picking arguments with political opponents, promote personal and party agendas, etc. It failed to stop the spread of Covid but has inflicted substantial and lasting damage.

Anatomy of the Banking Crisis of 2023

By Jeffrey Tucker

For three years, I’ve been amazed at the relative calm in the financial system. It truly did not seem believable to me that governments and central banks could utterly shatter all market functioning and flood the world with paper money and yet there be no structural consequences for the banks.

My only question was what would be the trigger and how would it unfold.

In retrospect, the whole thing is perfectly obvious.

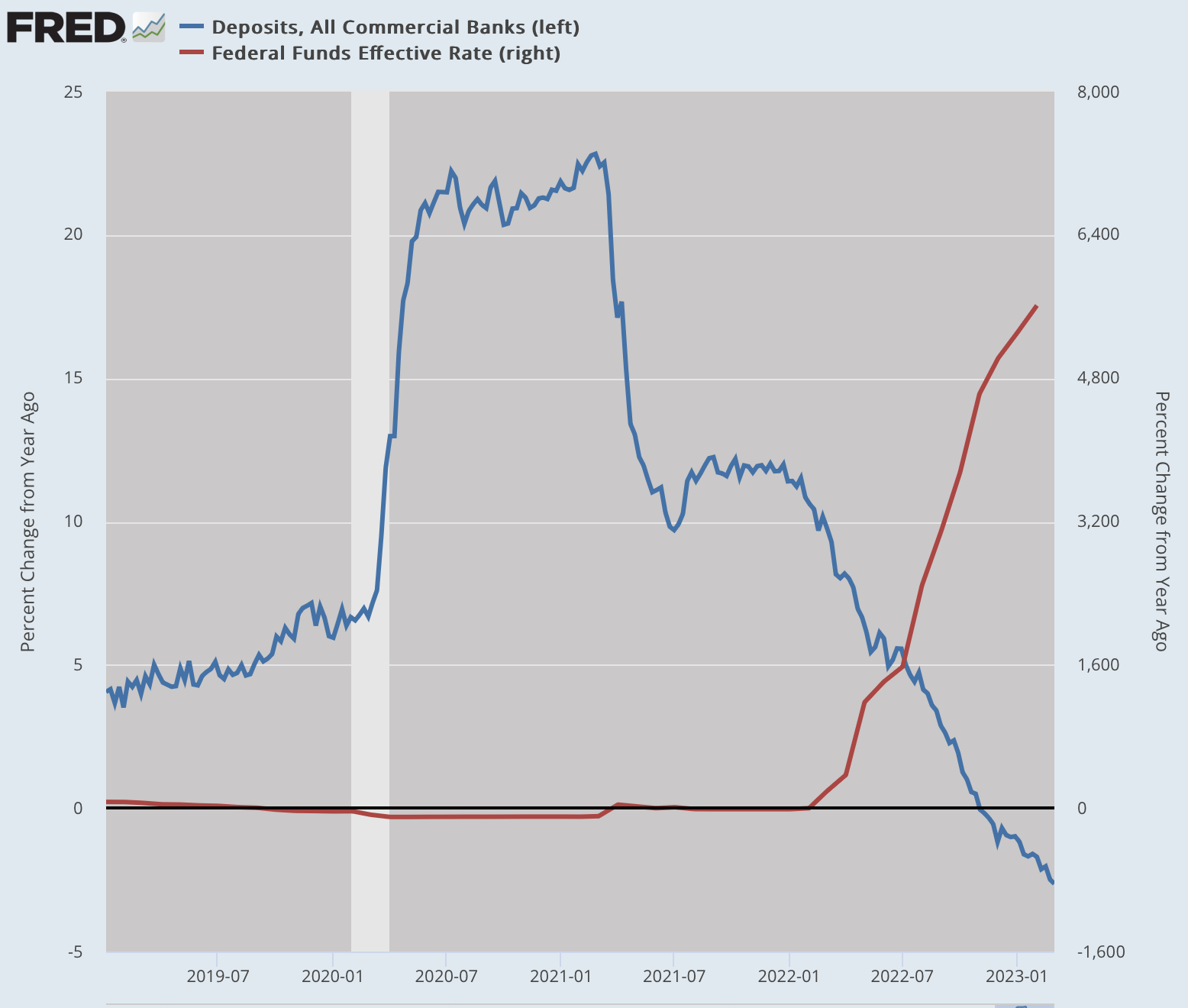

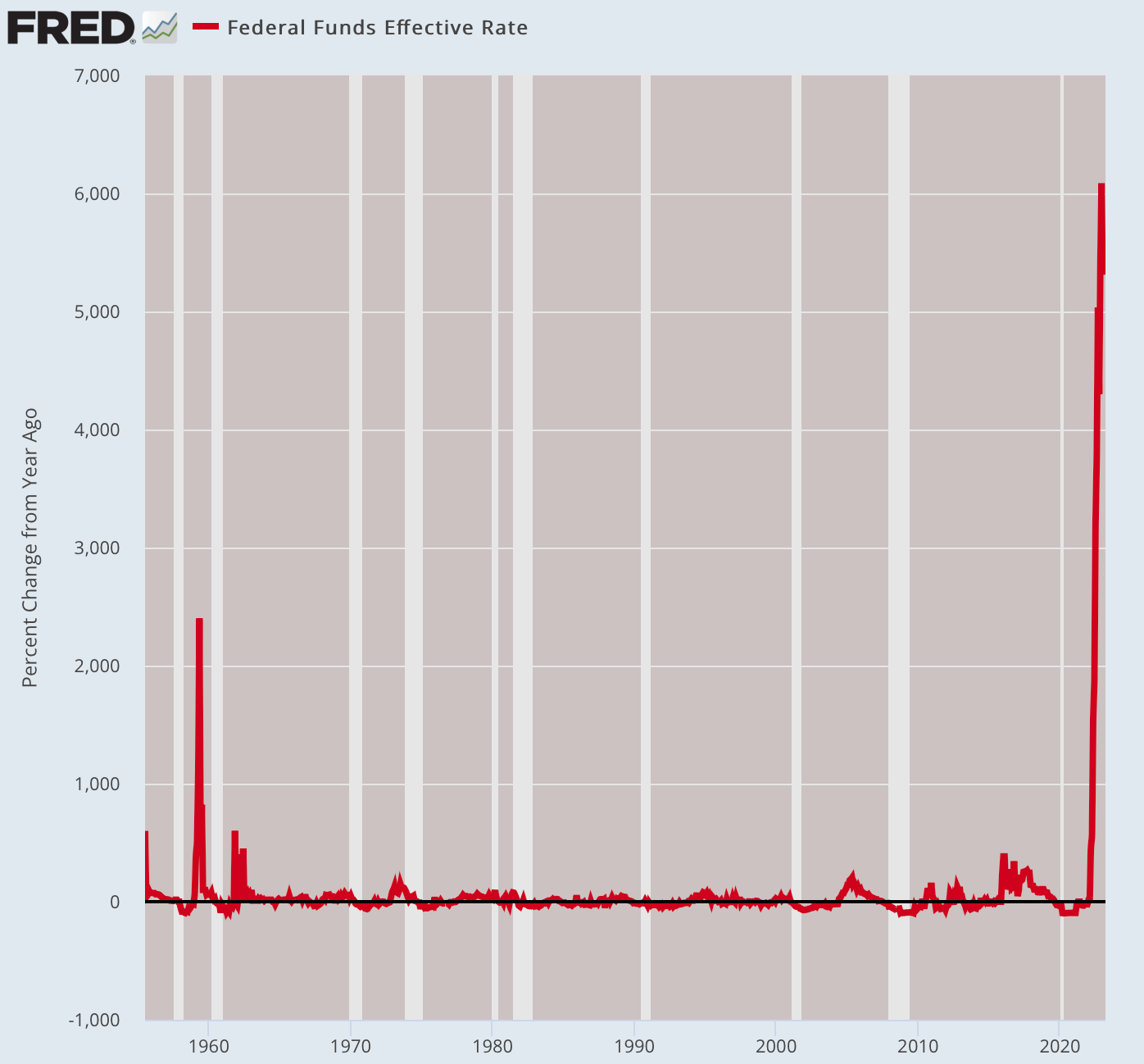

Between the first week of March 2020 and exactly two years later, the Federal Reserve printed $6.5 trillion, at some point reaching a per annum increase of 26 percent. We’ve never experienced anything like this before. It also represented a complete reversal of Fed policy, which had been attempting a tightening for the prior six months.

Fed chair Jerome Powell was attempting to reverse the disastrous policy of 2008 enacted by Ben Bernanke, which put a hard price control on interest rates. He drove them to zero, thus creating 12 years of production distortions in which money chased high-end information-based sectors and eschewed savings. It was a massive subsidy to leverage, and Powell knew that he had to change it.

Then the pandemic panic hit. He was called upon to play his role of counterfeiter-in-chief. Buying all the lies and baloney about the impending plague, he accommodated Congressional spending with the most irresponsible monetary policy one can imagine.

The new money was spread around the population with direct infusions of cash designed to mitigate the effects of lockdown. That began exactly three years ago today. Every amount of horror we’ve seen since then traces to that day.

Initially, the money seemed like a wonderful blessing. It always does. Savings soared to the heavens. It peaked at an astonishing 38 percent before plummeting again and reaching a rock bottom of 3.2 percent. Why? Inflation hit and the money ran out for American households and businesses.

But the new money was not destroyed of course. No amount of changed Fed policy could undo the damage. The Fed attempted to reverse course with higher interest rates. A furious and bitter Powell then tried to calm inflation with a repeat of Paul Volcker’s experience from the late 1970s.

But there was a huge difference. Powell was starting at zero. He had to chase down inflation rates reaching double digits. That would require the most brutal interest-rate increases in modern history. But he was all in. He wanted to be valorized in the history books as the man who killed the great inflation of 2021–22.

Backing up just a bit, let’s ask the question: where does this money end up? That’s an easy one. It landed in the banks. Bank deposits went from $13 trillion to $18 trillion in a mere two years. The banks were flush with cash. No one had ever seen anything like it.

The money had followed the predictable trajectory: from Congress to debt to Fed purchases of debt to U.S. citizens and businesses straight into the banks. Bank balances were rising by 23 percent at the height of this monetary bonanza.

This lasted until Powell turned off the spigots and drove rates extremely high. Then we whipsawed again and deposits left the system as individuals and businesses struggled to pay their now much-higher bills.

Just how extreme has Fed policy been? We have no records of anything like this. Again, remember that he was starting at zero and had to get to the terminal rate at or exceeding the rate of inflation. It’s a crude and brutal game but Powell was committed.

Now, think of yourself as a banker in the early days and the cash was flooding in. What’s to complain about? Nothing if one loans it out again but that was not really possible at this scale. There were no takers for the money under lockdown conditions, not any that were worthy of the risk in any case. So the banks needed a place to park their new-found wealth.

They could have rested it with short-term Treasuries but those were losing money in real terms simply because the inflation rate was running ahead of the return. The only attractive option was to store the bulk of the new deposits in fixed-rate long-term Treasuries: anywhere between 30 days and 30 years. Part of that also meant socking away deposits in

collateralized mortgage obligations and other products. That was where the money was to be made. They believed that they were making the right decisions for depositors and stockholders.

What happened when rates changed? The banks over time found themselves with a closet full of depreciated bonds. They were holding bonds at a fixed rate of 3 and 4 percent while the same products purchased new were earning 5 and 6 percent. There was simply no choice but to dump them and take a haircut, massively cutting into profits.

This would have been the safe and wise solution. But did they? Some did. Most did not. Some banks like Silicon Valley Bank just rested on their laurels, enjoying the Zoom life and making ads about social justice. When the crisis hit, they went belly up in a flash.

Keep in mind that they were just dealing with a devalued portfolio of assets. The higher rates also hit businesses very hard, particularly those that live on leverage. They started pulling out cash to cover the rising debt burden. That drained away reserves from the bank. But raising the money to cover their operations also meant selling their closet full of junk bonds at a deep discount. They waited too long.

Perhaps the damage could have been limited if the Biden administration had some backbone and just let the failing banks fail. Instead, like children and idiots, they promised the moon: all deposits at important financial institutions will be hereby guaranteed. It’s a promise essentially to print another $10–20 trillion should the need arise. The phrase “moral hazard” doesn’t entirely describe the extent of the policy disaster here.

Instead of calming markets, the Biden promise made it even worse. Everyone wanted to know just how sound the system really is. And the markets began to eye these bank valuations with grave skepticism. Suddenly everything was in question.

At last, the banking crisis arrived. It was right to long expect one but to perfectly foresee how it would happen was not entirely easy. As these things go, the unfolding of events is perfectly obvious in retrospect.

What can the Fed do now? It has no choice but to stay the course on its tightening, even as the Biden administration just promised the most irresponsible spending and printing policy in modern history. The two policies are at odds with each other. They make no sense at all.

What should happen? The banks that are in trouble need to die, contagion or not. There is no getting around the payment of a hugely heavy price for the biggest disaster in public-policy history, namely the decision three years ago today to lock down for a virus. You cannot wreck social and market functioning and expect that there is not a mean price to pay.

Yesterday, there was all sorts of talk about a new Great Depression. At this point, to predict such a thing is not very controversial. We would be extremely lucky to avoid one. Looking around at the banking and financial system, the leverage in households and businesses, and the instability in world trade in general, it truly does seem like our luck has finally run out.

Glad to hear more and more people are relying on Brownstone Institute. And, Jeffrey Tucker, thank you for the tour of the money flows of the last several years that you gave in your article Anatomy of the Banking Crisis of 2023.

Thank you for your post. The interesting thing is that the 16th March was after the 15th, the Ides of March. Beware the Ides of March.

https://alphaandomegacloud.wordpress.com/2023/03/16/beware-the-ides-of-march-15th-march-2023/